Polish Company Fenige Has Had Its License Revoked: What's Behind the Sanctions Against Major Fintech Companies

29 June 2026 19:15A wave of high-profile exposés and sanctions appears to be unfolding in Poland’s fintech market, though the final outcome remains highly uncertain.

Recently, the leader of the Polish fintech industry, Fenige, had its license revoked early, and the company's management, according to specialized Telegram channels, is likely being searched. One of the key reasons cited is alleged cooperation with Russia and involvement in processing transactions for the illegal Ukrainian and European gambling markets.

On the one hand, the actions of the Polish Financial Supervision Authority (KNF) regarding Fenige indicate tighter control over payment services and the fight against money laundering. On the other hand, the case has garnered significant attention because the company has grown steadily in recent years, posted record profits, and received EU grants to develop its projects.

UA.News examines the high-profile Fenige case, explores whether such sanctions could become a systemic trend for Polish and Ukrainian fintech, and shares the views of financial market experts on the matter.

Record Performance Since 2022 and New Ambitions

Poland’s Fenige is an example of the rapid rise of Central European fintech companies. The company operates in the field of card-based money transfers and domestic and international payments, serves the e-commerce sector, and acts as a primary acquirer for global payment systems.

Fenige uses its own payment processing platform, which is directly connected to the VISA and Mastercard systems. The company’s website states that Fenige specializes in “smart payment systems that help partners grow across Europe and beyond.” Fenige also receives co-financing from the European Union—the EU has provided grants for a number of its fintech projects.

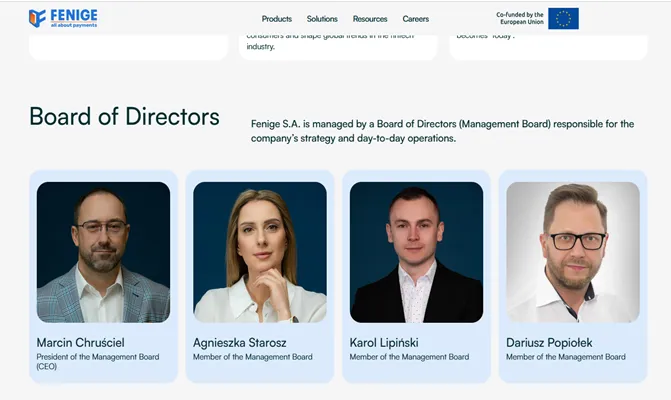

Fenige is governed by a Board of Directors, which is responsible for the company’s strategy and day-to-day operations.

In 2017, Fenige raised tens of millions of zlotys in several rounds of investment to fund its growth. In addition to private shareholders, its investors included major players such as WP2 Investments and Movens Capital.

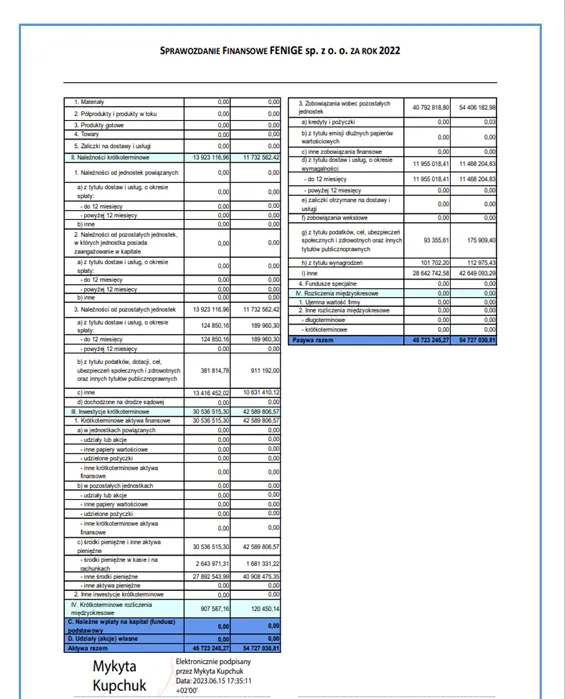

At the end of 2022, Fenige posted record results, processing over 3 million transactions totaling more than 545 million euros (2.4 billion zlotys). At that time, its year-over-year growth rate exceeded 70%, which impressed investors.

“Fenige’s revenue from transactions in 2022 significantly exceeded 11 million euros (50 million zlotys), representing impressive growth over the past five years. The path has been challenging, but the team has succeeded and successfully overcome all obstacles. Moreover, the company’s current performance demonstrates that it continues to deliver very strong results, and if future plans are implemented, positive trends in business development will be achieved in the long term. “We are very pleased with this investment and look forward to the future for Fenige and its team,” Movens Capital noted.

However, just one year later, in October 2023, Movens Capital announced that it was exiting Fenige, acknowledging that the return on investment from the project was 4.5 times the amount invested.

Photo: Marcin Chruściel, CEO of Fenige

In 2025, the company’s CEO, Marcin Chruściel, who has led Fenige since May 2022, stated in an interview with Polish business media that the company plans to continue its growth and achieve an average annual growth rate of 30%. This will be achieved primarily by entering the cross-border payments market.

“We are developing global withdrawal options across all existing payment systems. For example, a customer might contact us and say they’d like to withdraw funds to cards in China using China UnionPay, and we already offer that service,” Khruszel said, outlining the company’s plans.

First License Revocation

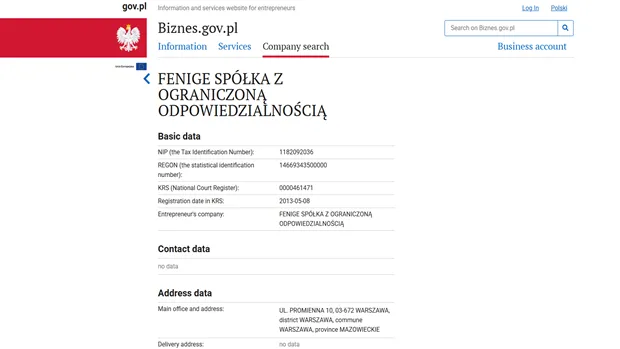

The fintech company, with a history spanning more than a decade, was originally named Fenige sp. z o.o. In 2023, it was renamed Fenige SA (a joint-stock company registered in the National Court Register under number KRS 0001057371).

Fenige received a national license for financial activities in August 2017 and has since operated as a payment institution licensed in the European Union under the supervision of the Polish Financial Supervision Authority (KNF). Fenige has also obtained certification under the PCI DSS (Payment Card Industry Data Security Standard).

However, in May 2019, the KNF temporarily revoked Fenige’s (then Fenige sp. z o.o.) license for payment services. According to the regulator’s findings, the company failed to ensure prudent and stable management of its operations in this area. Specifically, it did not complete the reauthorization procedure as required by updated legislation.

In the fall of 2020, the Commission revoked this decision, explaining that the license revocation was not final and was not subject to immediate enforcement. Following this announcement, Fenige filed a request for reconsideration, submitting additional documents.

KNF’s New Allegations Against Fenige

On June 25, 2026, it was reported that the Polish regulator, the KNF, had once again revoked Fenige’s license. The official reason cited was that the company had failed to ensure proper, stable, and prudent management of its payment services operations.

The Commission announced that once the decision takes effect, the company must cease providing payment services and entering into new contracts with customers. At the same time, Fenige was permitted to fulfill its existing obligations to customers and partners until September 30, 2026.

Until then, the company is required to ensure that customers can withdraw funds or transfer money to accounts at other financial institutions.

The Financial Supervision Authority revoked Fenige’s license to provide payment services as a domestic payment institution for failing to ensure prudent and stable management of its payment services operations: https://t.co/DF37za5FmE pic.twitter.com/S18XjkxRPJ

— KNF (@uknf) June 25, 2026

However, this time the case has taken on a new context. Preliminary reports suggest that one of the key reasons for the license revocation is the company’s alleged ties to Russian businesses and suspicions of involvement in processing payments for the illegal Ukrainian and European gambling markets. The final official conclusion of the Commission or the relevant regulatory authorities will reveal to what extent these theories correspond to reality.

Currently, the KNF is acting against the backdrop of a broader trend toward stricter regulations concerning fintech and payment service providers in Poland.

In particular, the current situation appears to be a continuation of a previous episode involving the revocation of the license of the fintech company Quicko, with which Fenige has business ties. In June of this year, the KNF revoked Quicko’s license, and the Polish Ministry of the Interior added it to its sanctions list due to its alleged involvement in a Russian sanctions-evasion scheme.

The company denied these allegations, emphasizing that no concrete evidence or information had been provided to confirm the execution of payment transactions with Russia or citizens of the Russian Federation, with the exception of residents of European Union member states.

“We would like to note that only approximately 0.1% of Quicko payment tool users (approximately 400 out of 400,000 Quicko customers) were of Russian origin, and all of them were EU residents,” the company said in a statement.

Expert comments on the revocation of Fenige’s license

Galina Heylo, President of the International Payment Association (IPA)

“This fact alone is very telling. It demonstrates that for the Polish regulator, a company’s size, its international partners, participation in European Union programs, or a significant market share are no guarantee of preferential treatment.

The financial sector operates on trust, so the regulator evaluates not the company’s commercial success but its compliance with requirements regarding corporate governance, risk management, protection of customer funds, compliance, and financial stability. If, in the supervisory authority’s opinion, these requirements are not met, it must apply the measures provided for by law, regardless of the market participant’s status.

At the same time, it is important to wait for the KNF’s full justification of its decision and the completion of all possible appeal procedures. Only then will it be possible to draw final conclusions regarding the specific grounds for revoking the license.

For the Polish market, this is first and foremost a signal of increased regulatory oversight. In recent years, European regulators have been paying increasing attention to issues of corporate governance, AML/CFT, operational resilience, and consumer protection. This trend is pan-European and applies to all financial institutions without exception.

This case is also of great significance for Ukraine. Ukrainian fintech companies that are operating in or planning to enter the European market must understand that compliance with European regulatory requirements is no longer a mere formality but a key competitive advantage. Investors, banks, and international payment systems are increasingly evaluating not only a business’s technological capabilities but also the quality of its risk management, internal control, and compliance systems.”

Pavlo Kotsyubynskyi, attorney

“The decision by the Polish regulator, the KNF, to revoke Fenige’s license is one of the harshest measures that can be imposed on a payment institution. At the same time, from a legal standpoint, it is important to clearly distinguish between the official grounds for the regulator’s decision and the information currently circulating in the media.

As indicated by the materials published by the KNF, the formal basis for revoking the license was the regulator’s assessment that the company failed to ensure proper, stable, and prudent management of its activities in the field of payment services. These are precisely the requirements set forth in Polish legislation, which is harmonized with European regulations governing payment institutions, and in the event of significant violations, they may constitute sufficient legal grounds for revoking a license.

At the same time, reports of the company’s possible ties to the Russian Federation or its involvement in processing payments for illegal gambling operations have not yet been established as legal facts. If these circumstances are not set forth in the reasoning section of the regulator’s decision or are not confirmed by the results of criminal proceedings or court rulings, they should be considered solely as matters under investigation, rather than as proven violations.

At the same time, the very fact of the license revocation indicates a clear tightening of the regulatory approach to the financial sector in Poland. Recent decisions regarding payment institutions demonstrate that European supervisory authorities are increasingly scrutinizing not only companies’ financial performance but, above all, the effectiveness of corporate governance, internal control systems, risk management, AML/CFT compliance, and the protection of customer funds. The scale of the business, international investors, or cooperation with global payment systems are no longer, in and of themselves, a guarantee of favorable treatment from the regulator.

Does the revocation of the license mean Fenige’s inevitable collapse? Not necessarily. However, this creates critical risks for the payment institution. The company effectively loses the ability to carry out its core licensed activities, enter into new contracts, and expand its business. Even if the law allows the company to fulfill its existing obligations to clients by a specified date, the reputational consequences, the loss of partners, and a decline in revenue could significantly impact its future operations.

At the same time, the legal process does not end there. Fenige has the right to appeal the KNF’s decision in accordance with the procedure established by law. It is precisely a judicial review that will allow for an assessment of whether the regulator’s conclusions were sufficiently substantiated and whether the principles of due administrative procedure and proportionality of the measure applied were observed.

A precedent already existed. In 2019, the KNF also revoked Fenige’s license; however, that decision was subsequently overturned after a review of the case materials and the submission of additional documents by the company. This indicates that the financial regulator’s decisions are not necessarily final and may be reviewed.

At the same time, it would be incorrect to automatically apply the 2019 situation to the current one. While the 2019 case primarily concerned reauthorization and administrative procedures, the current decision was made against the backdrop of significantly stricter European oversight of the financial sector, as well as efforts to combat sanctions evasion, money laundering, and the financing of illegal activities. That is precisely why the prospects for license renewal will depend not on the existence of a previous precedent, but on the substance of the evidence, the reasoning in the KNF’s decision, and the outcome of the court appeal.

For the Ukrainian fintech market, this case also sends an important signal. It demonstrates that regulators in both Poland and Ukraine are increasingly using the strictest enforcement measures against participants in the payments market. At the same time, the effectiveness of such oversight directly depends on adherence to the principles of the rule of law, due process, and a sufficient evidentiary basis. After all, the practice of both Polish and Ukrainian courts shows that even decisions by financial regulators can be overturned if they are based on assumptions rather than on proper and admissible evidence.”

Penalties Against Major Payment Systems in Ukraine

Perhaps by coincidence, in June of this year, Ukraine also announced strict sanctions against major payment systems. The NBU justified its decisions as part of its efforts to ensure the integrity and transparency of the financial services market.

The two largest payment terminal networks—EasyPay (FC “Kontraktovy Dom” LLC) and City24 (Swift Garant LLC)—received massive fines from the NBU: 135 million UAH each. The official reason sounds complicated: “improper organization of primary financial monitoring.” Simply put, the National Bank believes that the companies failed to adequately verify the origin of the funds passing through their terminals.

However, when considering the technical nuances and market realities, the situation does not seem so clear-cut. Some Ukrainian media outlets have speculated that the high-profile announcements about the “fight against dirty cash” totaling 270 million hryvnia may be part of a larger administrative and media strategy. And the NBU’s tough measures could indicate that the regulator is going beyond the scope of ordinary supervision.

Before the fines were announced, the media actively circulated information alleging that these terminal networks were linked to businessman Timur Mindich and the high-profile “Midas” case. However, the actual facts suggest that there is most likely no legal or financial connection between EasyPay, City24, and the individuals involved in the investigations. And this whole story appears to have been built on conspiracy theories and the “six degrees of separation” principle.

Legal Precedents: When the NBU Loses Due to Subjectivity

The astronomical fines give the impression that the National Bank is always right. However, Ukrainian judicial practice shows that the regulator often loses to financial institutions when its inspectors are guided by their own assumptions rather than the letter of the law.

According to our sources at the NBU, lawyers within the agency itself are well aware of the risks: if they act purely on emotion or based on internal instructions that contradict the law, the courts will completely overturn such decisions.

There are plenty of examples:

The “RVS Bank” case: The Supreme Court at the time completely overturned the NBU’s fine for alleged violations of financial monitoring, ruling that officials had not acted in a manner prescribed by the Constitution.

The dispute with the “International Investment Bank”: The National Bank attempted to collect 20.5 million UAH from the bank for “shortcomings in customer verification,” but the appellate court found the auditors’ claims to be biased and overturned them.

The WayForPay case: The popular payment system also had to go to court to defend its license against discriminatory actions by regulatory authorities.

These cases clearly demonstrate that vague “financial monitoring” rules can sometimes be used as a tool to exert selective pressure on the private fintech sector.