A French court has found Worldpay complicit in fraud: implications for the fintech industry

24 June 2026 16:00On June 9, a Paris court found the global payment system Worldpay guilty of providing services to illegal financial brokers who operated using a classic scheme: fake websites, promises of high returns, and defrauding investors. The company was fined 200,000 euros.

The case against Worldpay has become one of the most significant legal proceedings in recent years for the European fintech sector. For the first time, a major international payment processor was held criminally liable for failing to adequately monitor a client who used its infrastructure to commit fraud.

UA. News details this exceptional case and its impact on strengthening accountability in the fintech industry.

How the Global Fraud Scheme Operated

At the center of the investigation was a large-scale online fraud scheme in the Forex market that operated from 2011 to 2014. What makes this case unique is that approximately 12–15 years passed between the time the fraud was committed and the court’s verdict.

The case materials indicate that the perpetrators created fake investment platforms and currency trading websites, promising high returns to private investors. Potential victims were recruited through online advertisements and phone calls.

Investors believed they were investing in the currency market, expecting high returns. In reality, their money was not invested but was siphoned off through a network of accounts around the world. The total losses suffered by the French investors are estimated at at least 35 million euros.

During the investigation, French law enforcement officials discovered that a significant portion of the payments passed through Worldpay’s infrastructure.

A key link in the chain was Seroph (a Cyprus-based company), which provided services to fraudulent brokerage platforms and used Worldpay’s payment solutions to launder funds. The court determined that over 16.8 million euros were transferred through these channels.

The indictment noted that these crimes led to many tragedies. Among the victims were retirees who lost a significant portion of their savings, as well as individuals who borrowed money in hopes of improving their financial situation.

In total, after more than ten years of judicial investigation, the cases of eleven defendants—nine individuals and two companies, including Worldpay—were referred to criminal court.

Five of the defendants—including the company Seroph—entered into a plea agreement (CRPC) in January 2026.

Worldpay’s Structure and the Charges Against It

Worldpay, an American multinational fintech company, specializes in processing payments for businesses around the world. It processes over $2.3 trillion in transactions annually for leading global brands and provides services in more than 175 countries. It supports 135 national currencies. The company’s main office is located in Cincinnati, Ohio (U.S.), with an international headquarters in London and 40 offices in 25 countries.

“Worldpay processes billions of transactions for the world’s largest brands. We take care of all the challenges so you can focus on growth,” the company’s website states.

Paradoxically, one of the key services promoted by this payment giant is “the security of every transaction through an advanced fraud detection and authentication system.”

The key figure and CEO of Worldpay is Charles Drucker. Until 2018, he served as CEO of Vantiv (an American company that acquired Worldpay in 2017 and adopted its name for the combined entity). Charles Drucker joined Vantiv in 2004 and led the company’s spin-off from Fifth Third Bancorp in 2009.

Previously, Charles Drucker served as president of Fifth Third Processing Solutions and had extensive experience in the investment advisory division, which encompassed private banking, retail securities brokerage, asset management, and institutional services.

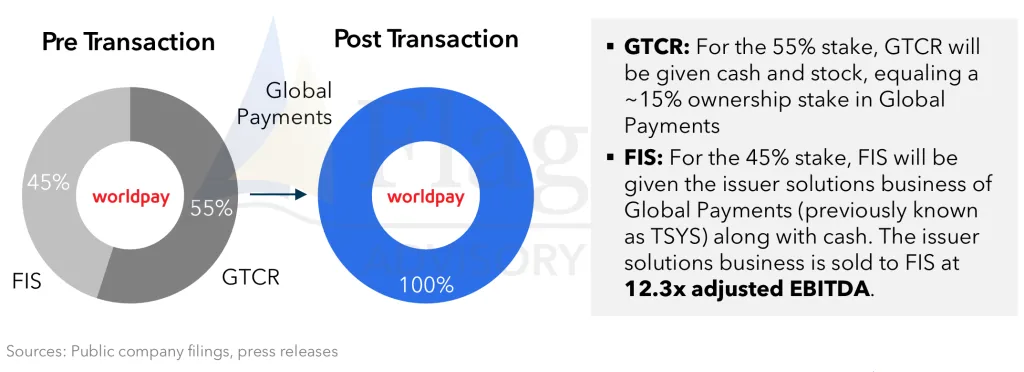

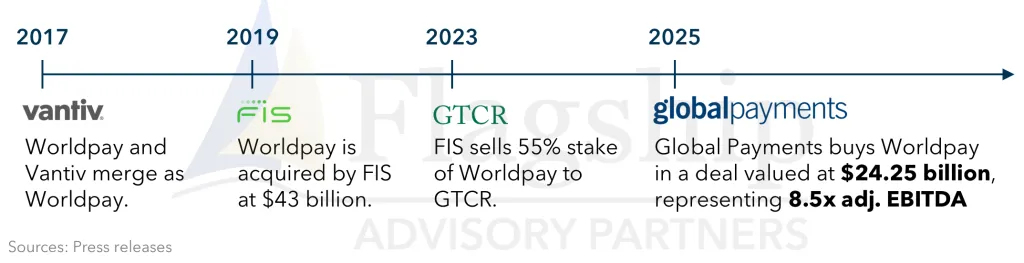

In January 2026, Global Payments announced the acquisition of 100% of Worldpay’s shares for $24.25 billion.

The previous shareholders—private equity firm GTCR (which owned 55%) and fintech corporation FIS (which owned 45%)—sold their stakes and transferred full ownership to Global Payments.

Worldpay’s history of mergers and acquisitions (M&A) in recent years has unfolded as follows:

FIS initially acquired Worldpay in 2019 for $43 billion, making it one of the largest deals in the payments industry.

In 2023, FIS sold a controlling stake (55%) to GTCR.

Worldpay was sold to Global Payments at a price 8.5 times its adjusted EBITDA (the deal was valued at $24.25 billion).

In March 2026, Worldpay faced two separate lawsuits in court related to Seroph, a company suspected of financial fraud. The prosecution’s position was that Worldpay:

failed to conduct proper customer due diligence (KYC/AML);

failed to verify the legality of Seroph’s operations in France;

ignored signs that funds from illegal investment schemes might be passing through its payment infrastructure.

Consequently, the court found the Worldpay payment system to be an accomplice in the illegal provision of services and ordered it to pay two fines of 100,000 euros each.

As for the organizers of the scheme, who were identified in France and Israel, the court handed down significantly harsher sentences—up to 3 years in prison and fines of up to 400,000 euros.

New Liability for Payment Platforms

The significance of this case lies in the fact that the payment service provider—without whose involvement it would have been impossible to defraud investors—was placed in the dock alongside the perpetrators. Until now, regulators have primarily punished the direct organizers of financial scams.

For the financial industry, this sets a precedent for a new level of liability. For the first time, a French court has found a payment processor guilty of failing to adequately vet a merchant (a legal entity in the fintech sector). This sets a legal precedent for similar cases in other jurisdictions.

Lawyers also point to the risk of retroactive application, as the case concerns transactions from 2011–2014, while the court’s verdict was handed down in 2026. This means that regulators can hold entities accountable for proven crimes even decades later.

And although a fine of 200,000 euros is a negligible amount for a global-scale processor, the case causes reputational damage and carries significant weight for the market.

It also changes the approach taken by organizers of fraudulent schemes who, operating from other jurisdictions, use shell companies and disappear before victims have a chance to receive compensation. Under such circumstances, opportunities for recovering losses were extremely limited.

According to legal experts, the ruling against Worldpay marked the end of an era in which payment systems could position themselves as neutral technology platforms. Investigators will now focus not only on the direct perpetrators of fraud but also on entities that may have intentionally or unintentionally facilitated these crimes.

The Paris court has effectively tightened requirements for the industry: if a fintech company earns revenue from processing payments, it must not only execute transactions but also thoroughly verify that no fraudulent scheme is behind them.

Banks and payment aggregators will be forced to tighten their verification procedures when onboarding business entities, particularly in the financial sector. This fundamentally disrupts the structure that has developed in the financial services market over many years, when payment providers widely worked with Forex brokers, CFD platforms, and other high-risk segments due to high commissions. Following the Worldpay ruling, many companies will have to either stop working with such clients or impose stricter requirements on them.