The National Bank of Ukraine set a lower official exchange rate for the dollar and the euro on July 2. The U.S. dollar lost a few more kopecks, and the euro also continued to depreciate. Against the backdrop of these changes, Ukrainians are increasingly wondering what is more profitable right now—keeping their money in foreign currency or putting it in a deposit account.

NBU Exchange Rates

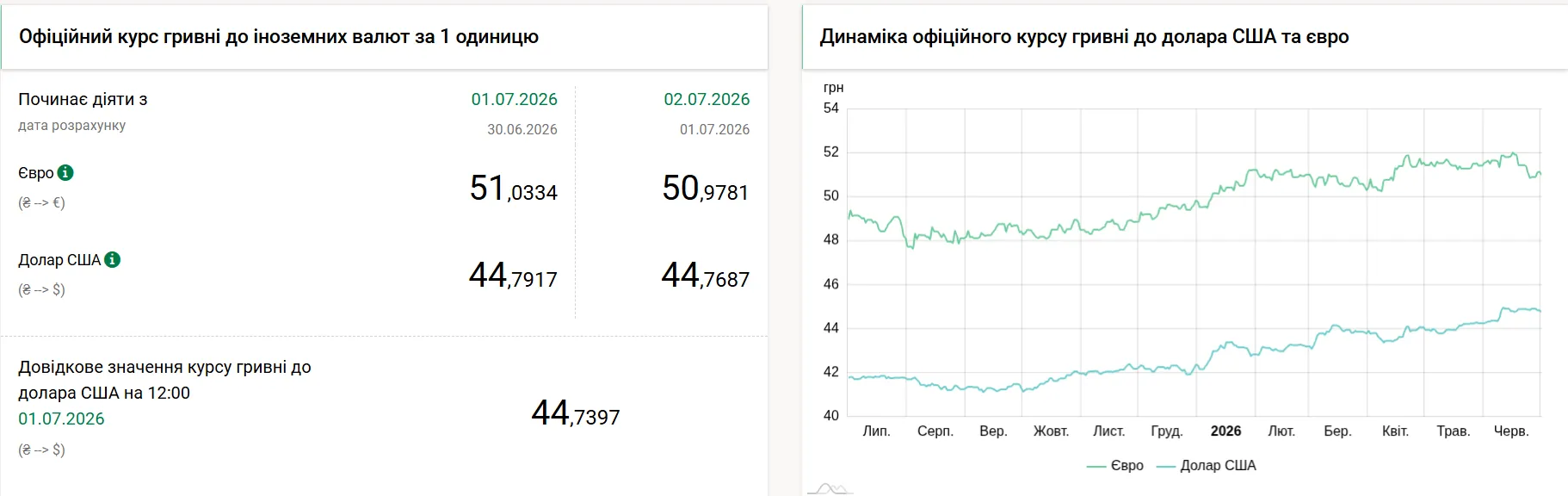

On July 2, the NBU set the official exchange rate for the dollar at 44.76 hryvnia, which is 3 kopecks lower than the previous day. On July 1, the official exchange rate was 44.79 hryvnia per dollar.

At the same time, the official euro exchange rate also fell. The regulator set it at 50.97 hryvnia, which is 6 kopecks less than on the previous banking day. The day before, the euro exchange rate stood at 51.03 hryvnia.

Thus, at the beginning of July, the official exchange rates for both major currencies continue to gradually decline.

Should you buy foreign currency now?

As Serhiy Mamedov, vice president of the Association of Ukrainian Banks and chairman of the board of Globus Bank, told RBC-Ukraine in a comment, one should not think in terms of “either all in dollars or all in hryvnia.”

According to him, in the context of the war, the wisest strategy remains diversifying one’s savings.

“It’s certainly possible to keep part of your funds in foreign currency as a reserve. This is psychologically understandable and financially justified if it’s a reserve for unforeseen events. But buying up foreign currency solely out of fear and based on rumors is, to put it mildly, not the best strategy,” the banker explained.

At the same time, he noted that hryvnia deposits remain quite attractive thanks to the NBU’s high discount rate. Average deposit rates start at approximately 14% per annum, while the highest rates can reach 16.5–17.5%.

According to Mamedov, if you place 100,000 hryvnias in a deposit at 14% per annum for six months, you can earn about 5,400 hryvnias in net income after taxes. For buying dollars to yield a similar result, the exchange rate would have to rise to approximately 47.4 hryvnia per dollar, and with higher deposit rates—to nearly 48 hryvnia.

Therefore, the expert emphasizes, if the hryvnia weakens gradually rather than in sharp jumps, a deposit may prove more profitable than passively holding foreign currency.

At the same time, the optimal approach remains a combination of various savings instruments. A portion of funds can be held in hryvnia deposits or government bonds, another portion in foreign currency, and a certain amount of cash or funds can be kept in a card account.